Ci spiace, ma questo articolo è disponibile soltanto in English.

Dipartimento di Economia e Giurisprudenza

Via S.Angelo Loc. Folcara, Cassino (FR)

Room 2.20

Ingresso libero

Thursday, April 21

10.00 – 10.30 Antonella Stirati

Non-mainstream interpretations of the changes in functional income distribution – some critical considerations

10.30 – 11.00 Antonio Bianco & Claudio Sardoni

Banks and finance in contemporary macroeconomics: advances, limits and contradictions

11.00 – 11.30 Sergio Cesaratto

Initial and final finance in the monetary circuit and the theory of Effective Demand

11.30 – 11.45 Coffee break

11.45 – 12.15 Pasquale Tridico & Riccardo Pariboni

Inequality and financial crises: a theoretical assessment

12.15 – 12.45 Echkard Hein

Autonomous government expenditure growth, deficits, debt and distribution in a neo-Kaleckian growth model

12.45 – 14.30 Lunch

14.30 – 15.00 Matteo Deleidi

Money endogeneity in the Eurozone

15.00 – 15.30 Lino Sau

Coping with deflation in the euro-zone

15.30 – 16.00 Daniel Detzer

Financialisation, Debt and Inequality: Export-led Mercantilist and Debt-led Private Demand Economies in a Stock-flow consistent Model

16.15 – 16.30 Gennaro Zezza

Financial balances and macroeconomic closures in the long-run

16.30 – 17.00 Dario Togati

Financialization and stagnation

17.00 – 17.30 Eckhard Hein

Secular stagnation or stagnation policy? Steindl after Summers

Contributions

Antonio Bianco & Claudio Sardoni, Università di Roma “La Sapienza”

Banks and finance in contemporary macroeconomics: advances, limits and contradictions

ABSTRACT

No satisfactory analysis of the working of modern market economies can be carried out without giving due attention to the actual ways financial markets and the ‘real’ economy are related. The expanding macro-financial literature is facing a number of analytical challenges. A ‘arguably more fundamental’ (Borio 2014) deals with the nature of money supply and hence the theory of bank lending underlying such models. The conventional take on how changes in base money (monetary policy) are reflected in changes in money supply is the money multiplier doctrine. This is based on the understanding of banks as intermediaries of loanable funds (reserve assets) and lending as transfer of excess reserves. According to this (ILF) theory, money is created when banks borrow, and how larger the money supply is than the monetary base critically depends on savers’ willingness to hold bank money, rather than base money, in reserve. An alternative theory of bank lending (‘financing through money creation’, FMC) suggests that bank lending involves no intermediation at all since, when lending, the bank creates its own funding—most of bank deposits do not consist of cash paid in, but of credits borrowed (inside money), indeed. The limits banks face to money creation are economic, not technical: when extending loans, banks are liable to face a decline in reserves. The associated increase in liquidity risk can by covered by non-self-produced liquid funds (non-inside money). We consider the different (ILF and FMC) perspectives over bankers’ decisional problems and their different impact on the so-called financial cycle. From this we highlight some major differences in policy perspective and implications.

Sergio Cesaratto, Università di Siena

Initial and final finance in the monetary circuit and the theory of Effective Demand

ABSTRACT

One remarkable aspect of modern heterodox theory is the detachment between demand-led growth models and endogenous money theories. This paper suggests a possible integration of the Keynesian theory of the multiplier (and supermultiplier) with endogenous money and Keynes’s finance theories. Focusing upon Graziani’s version of the Monetary Circuit Theory (MCT), the paper is a contribution towards reconciling the preoccupation of MCT with initial production financing, and the concern of demand-side oriented heterodox growth theories with final financing of autonomous demand. Following Davidson, Dalziel and others, the paper shows that endogenous money finances production decisions based, inter alia, on expected consumption and investment orders. In turn, the income (super)multiplier generates actual consumption and saving. The latter funds the actual purchase of investment goods. The (super)multiplier is the nexus between initial and final finance. Various complications of this basic idea not yet considered by the literature are examined.

Matteo Deleidi, Università Roma Tre (PhD candidate)

Money endogeneity in the Eurozone

ABSTRACT

The paper investigates the relationship between enterprises’ credit demand and the interest rate. From a theoretical stand point, mainstream economists as well as scholars belonging to the Keynesian tradition advocate that changes in interest rates have positive effects on firms credit demand. From a Keynesian perspective, a downward sloping enterprise credit demand curve can be argued as a direct consequence of the existence of a negative relationship between the interest rate and investments demanded by firms (demand for capital goods). The negative relation between interest rates and the investment demand could be explained by the schedule of the marginal efficiency of capital, a mainstream inheritance absorbed by the Keynesian view. On the other hand, an alternative standpoint argues the investments does not depend on the level of interest rate but on the level of the aggregate demand that determines the capital goods demand even in the long-run.

Empirically, by applying a VAR and VECM methodology, this thesis proposes an analysis of the relationship between different types of credit provided by commercial banks and the respective interest rates. The econometric analysis is conducted on Europe as a whole, using aggregated monthly time series data (January 2003 to June 2015) provided by the ECB database, i.e., the amount of bank credit provided (i) to enterprises; (ii) for the purchase of houses; and (iii) for the purchase of consumption goods, along with the corresponding interest rates applied by commercial banks. The main results of the empirical analysis show a negative relationship between the interest rates and the credit provided by banks for the purchase of houses and of consumption goods. Conversely, no relationship was found between bank loans provided to enterprises and the respective interest rates. As a conclusion, this thesis maintains that changes in the interest rates cannot stimulate the enterprise credit demand aimed at financing investment.

Daniel Detzer, Berlin School of Economics and Law

Financialisation, Debt and Inequality: Export-led Mercantilist and Debt-led Private Demand Economies in a Stock-flow consistent Model

ABSTRACT

In the era of financialisation, increasing income inequality could be observed in most developed and many developing countries. Despite these similar developments in inequality, the growth performance and drivers for growth differed markedly among countries, allowing clusters of different growth regimes to be identified. Among them two extreme types: the debt-led private-demand boom type and the export-led mercantilist type. Whereas the former relies mainly on credit-financed household consumption in order to compensate for the potential lack of demand (associated with the depressing effect of financialisation), the latter relies on net exports as the main driver of aggregate demand. Using a stock-flow consistent model it will be demonstrated how increasing inequality, depending on a countries institutional structure and regulatory framework, affects growth differently, explaining the occurrence of both regime types.

Eckhard Hein, Berlin School of Economics and Law

Autonomous government expenditure growth, deficits, debt and distribution in a neo-Kaleckian growth model

ABSTRACT

This paper is linked to some recent attempts at including a non-capacity creating autonomous expenditure category as the driver and determinant of growth into Kaleckian distribution and growth models. Whereas previous contributions have focussed on taming Harrodian instability, generated by the deviation of the goods market equilibrium rate of capacity utilisation from a normal or target rate of utilisation, we rather focus on the so far neglected issues of deficit, debt and distribution dynamics in such models. For this purpose we treat the growth of government expenditures on goods and services, financed by credit creation, as the exogenous growth rate driving the system. We examine the medium-run convergence of the system towards such a growth rate, analyse the related long-run debt dynamics and deal with stability and income distribution issues. Finally we touch upon the economic and, in particular, fiscal policy implications of our model results.

Secular stagnation or stagnation policy? Steindl after Summers

ABSTRACT

The current debate on secular stagnation is suffering from some vagueness and several shortcomings. The same is true for the economic policy implications. Therefore, we provide an alternative view on stagnation tendencies based on Josef Steindl’s contributions. In particular, Steindl (1952) can be viewed as a pioneering work in the area of stagnation in modern capitalism. We hold that this work is not prone to the problems detected in the current debate on secular stagnation: It does not rely on the dubious notion of an equilibrium real interest rate as the equilibrating force of saving and investment at full employment levels, in principle, with the adjustment process currently blocked by the unfeasibility of a very low or even negative equilibrium rate. It is based on the notion that modern capitalist economies are facing aggregate demand constraints, and that saving adjusts to investment through income growth and changes in capacity utilization in the long run. It allows for potential growth to become endogenous to actual demand-driven growth. And it seriously considers the role of institutions and power relationships for long-run growth—and for stagnation.

Lino Sau – Università di Torino

Coping with deflation in the euro-zone

ABSTRACT

After an absence of almost half a century, the ghost of deflation is once again the main worry of central bankers and ministries of finance, in Japan for at least the last two decades and, more recently, in Europe Eurostat index shows that inflation dropped to 0.9% for the euro zone as a whole since September 2013. That is way under the European Central Bank (ECB) target which is close to 2%.

The recent renewed concern with deflation is then due in part to the historical association of deflationary episodes with financial crises, recession, stagnation and even depression. It is also prompted by the fear that in deflationary conditions, nominal interest rates may come close to their “lower bound of zero”, at which point monetary policy is thought to lose most if not all of its effectiveness.

Recently economists working in the conventional arena are muscling on deflation (Shiller, 2013; Goetz, 2005; Rogoff et al., 2003; Svensson, 2003). The timing of the renewal of mainstream scholarly and political concern with, and interest in deflation, is surprising after a long silence. As I try to stress in this paper, the belated “discovery” of the problems of deflation by the mainstream, as well as the economic policies suggested, are not convincing.The paper is structured thus: in section 1, I begin with a discussion on the causes and consequences of deflation, looking back to the founding fathers of the debt deflation school (i.e Keynes-Fisher-Minsky); in section 2, I scrutinize the fact that deflation, accompanied by a liquidity trap, may be the “nightmare” of economic policy makers; in section 3, I try to compare and contrast the economic policies suggested by the conventional approaches and by post-keynesians to avoid and to escape from a debt deflation spiral cum liquidity trap; in section 4, I get my conclusions.

Antonella Stirati, Università Roma Tre

Non-mainstream interpretations of the changes in functional income distribution – some critical considerations.

ABSTRACT

The last 30 years have witnessed a dramatic change in the distribution of income, with the wage share falling in all major industrialized countries. In addition, The wage-share data tend to under-estimate the actual changes in distribution, since the wage share comprises the salaries of top-managers, which rose sharply particularly in the Anglo-Saxon countries and which may be regarded as capturing part of business profits rather than as labour incomes.

To clear the ground it must also be clarified that these changes cannot be attributed, even partially, to an increase in the ratio of the value of the capital stock to value added, which is not shown in the data.

The interpretation of such changes in income distribution represents a challenge to economic analysis.

The Keynesian-Classical approach to the determination of distribution and employment presents an advantage in the explanation of the phenomenon with respect to mainstream approaches, consisting in the fact that it entails no a priori causal connections between the changes in the proportion between labour and output, or between the value of the capital stock and the value of output and the changes in distribution.

Yet both economic analysis and empirical observation may pose some questions also to the interpretations of the changes in distribution that have been advanced in the heterodox literature. The paper will explore some of the ways in which such changes have been interpreted outside the mainstream and critically assess them, with particular reference to US data. My limited purpose will be more that of framing the questions rather than finding the answers. This on the basis of some consideration on theory and empirical evidence which is by no means meant to provide a ‘test’ for theory, but rather to contribute to an initial reflection on the open questions.

Dario Togati, Università di Torino

Financialization and stagnation

ABSTRACT

…

Pasquale Tridico & Riccardo Pariboni, Università Roma Tre

Inequality and financial crises: a theoretical assessment

ABSTRACT

The objective of this paper is to critically assess the current literature on the circular relationship between inequality and financial crises, in order to establish a possible direction of causality. In recent years, advanced economies experienced dramatic changes in income distribution, the degree of financialisation and labour market institutions (Barba and Pivetti, 2009; Tridico, 2012; Kumhof et al., 2015; Stockhammer, 2015), which eventually led to an increase of the financial instability and to the burst of the bubble previously fed by decades of massive indebtedness.

This paper will offer a wide view of the different hypotheses on the topic of inequality and financial crisis from a theoretical point of view. As a first step, we will provide a discussion of the determinants of inequality, arguing that increases in labour flexibility, the weakening of labour market institutions and financialisation are major explanatory factors.

Finally, we will explore whether indebtedness, which emerged as a consequence of wage stagnation, and the related credit-led growth, can be a feasible and sustainable growth strategy in the long-run for advanced economies.

Gennaro Zezza, Università di Cassino e del Lazio Meridionale

Financial balances and macroeconomic closures in the long-run

ABSTRACT

Models addressing growth in the very long run are becoming relevant, in particular to help evaluate the impact of long-term shifts in climatic change, availability of natural resources, etc. The major example is given by the Shared Socio-economic Pathways projected up to 2100. Existing projections rely on neoclassical growth models, and heterodox alternatives are potentially relevant, in that they would provide a better way to handle uncertainty, and the role of the financial sector on growth. In this paper we challenge the existing macroeconomic closures in neoclassical growth models, which assume that all countries will extinguish their foreign and public debts in the long run. We propose an alternative based on the work of Godley, suggesting that governments should target their debt relative to the desire of the public sector to hold financial wealth, and that the countries’ net investment position will depend on which currency is used as international reserve.

We also discuss the implications of our proposal for the current policy debate in the Eurozone.

Dal sito dell’Associazione Economia per i cittadini, il secondo video, su crisi e neoliberismo.

Thomas Piketty ha presentato il suo best-seller Capital in the 21st century alla New School in New York.

Piketty ha presentato i risultati principali della sua ricostruzione storica della distribuzione dei redditi e della ricchezza in diversi Paesi. Ha scelto di evitare i punti che sapeva controversi – data la sede in cui discuteva – e anzi ha accennato più volte alla teoria mainstream secondo cui la concentrazione dei redditi premia gli skills, per negare che possa spiegare una quota consistente della concentrazione di redditi e ricchezza in atto negli Stati Uniti e in Europa negli ultimi trenta anni.

Su due punti Piketty ha inistito, e trovo entrambi convincenti. Il primo è che l’introduzione di una tassa sul reddito ha consentito di avere statistiche sui redditi personali che prima non erano rilevate. L’introduzione di una tassa sulla ricchezza, inclusa la ricchezza finanziaria, costringerebbe i governi a farla finita con il segreto bancario, e avremmo a disposizione statistiche sulla distribuzione della ricchezza, indispensabili a valutare eventuali politiche redistributive.

Il secondo punto riguarda l’incompatibilità tra la concentrazione dei redditi e la democrazia. Piketty ha sostenuto che le elevate aliquote marginali adottate dagli Stati Uniti prima, e da alcuni Paesi europei poi, erano all’epoca (anni ’70) considerate un requisito per evitare che un sistema democratico si trasformasse in una plutocrazia.

Anwar Shaikh ha deluso chi si aspettava una critica a Piketty sul concetto di “capitale”, e ha invece mostrato come le sue ricerche sulla distribuzione del reddito possano fornire un supporto teorico ai dati di Piketty.

Ha anche sottolineato il fondamentale contributo dato da Piketty nel pubblicare tutti i suoi dati su internet.

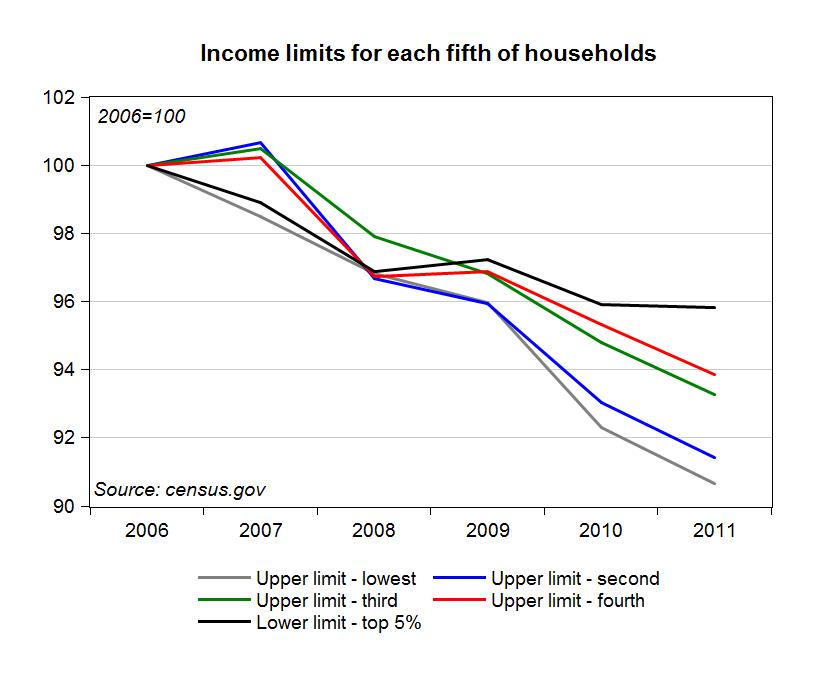

Il grafico, tratto dalla mia presentazione a Cambridge su “fiscal and debt policies for the future” di qualche settimana fa, riporta gli ultimi dati disponibili su una misura della distribuzione del reddito negli Stati Uniti. Le prime quattro linee rappresentano il limite superiore dei quintili di reddito, a prezzi del 2011, e l’ultima rappresenta il limite inferiore del 5% a reddito più alto, tutte rapportate alla stessa misura nel 2006.

Come si vede, la Grande Recessione ha ridotto il reddito in tutti i quintili, ma chi ha un reddito più alto è riuscito a perdere meno di tutti. Ad esempio, l’americano con reddito più alto nel primo quintile guadagnava $1860/mese nel 2006, ed è sceso a $1688, mentre l’americano con reddito più basso nel primo 5% guadagnava $16.175/mese, ed è sceso “solo” a $15.500 (il tutto misurato ai prezzi del 2011, ossia senza tener conto dell’inflazione).

Che i risultati di Reinhart e Rogoff fossero ridicoli, anche prima che si scoprissero gli errori di calcolo, era evidente a chiunque riflette sugli effetti distributivi delle politiche macroeconomiche… ora se n’è accorto anche Krugman.

Chissà quanto ne è consapevole Saccomanni. Proporre tagli e meno tasse vuol dire ridurre subito e con certezza il lavoro creato dal settore pubblico, e sperare che meno tasse producano maggiore domanda, maggiori vendite, e posti di lavoro: un processo incerto. E tagli alla spesa pubblica e meno tasse avranno prevedibili effetti distributivi.